.jpg)

The Digital euro: A threat or an opportunity for Belgian retail banks?

It is now official: the Digital euro has cleared its next major political hurdle. On Tuesday, June 23rd, the European Parliament’s Economic and Monetary Affairs (ECON) Committee approved its position on the file with a clear majority, paving the way for a final political agreement by the end of the year. This sets the stage for the ECB Governing Council to move forward at full speed with the launch of a 12-month pilot in the second part of 2027 (ECB, 5/3/26), aiming at a fully operational rollout by 2029.

At first sight, the path looks clear. However, the external reactions are much more nuanced. Febelfin, the Belgian financial federation representing the sector, has already warned about the potential detrimental effects of the new infrastructure on the current ecosystem. Among the main trouble spots, great uncertainty remains around the structural costs at stake and who exactly will foot the bill to bring the technology to the Eurosystem.

The so-called retail Central Bank Digital Currency (CBDC), or Digital euro, is central bank money in digital form, a twin of cash. Hence, the Digital euro will be different from commercial bank money — euros that most European citizens receive in the form of a salary, hold in their bank accounts and use to pay for groceries and bills. It will have the core features of physical cash, meaning legal tender status and a direct claim on the Central Bank — both of which commercial bank money lacks. The Digital euro is therefore essentially an attempt to digitise cash and, by doing so, strengthen the Central Bank’s role in the economy amid rising geopolitical tensions. It is about regaining monetary sovereignty and building “strategic autonomy” by reducing the EU's heavy reliance on non-European card giants like Visa and Mastercard.

Such an initiative will have a significant impact on the main related economic actors: banks, payment service providers (PSPs), merchants and consumers. It will certainly create interesting opportunities to innovate and improve the current model, particularly through AI. Before that, however, this might trigger considerable costs notably due to the major infrastructure changes that are required to support the rollout.

The Price of Building Europe’s Digital Cash

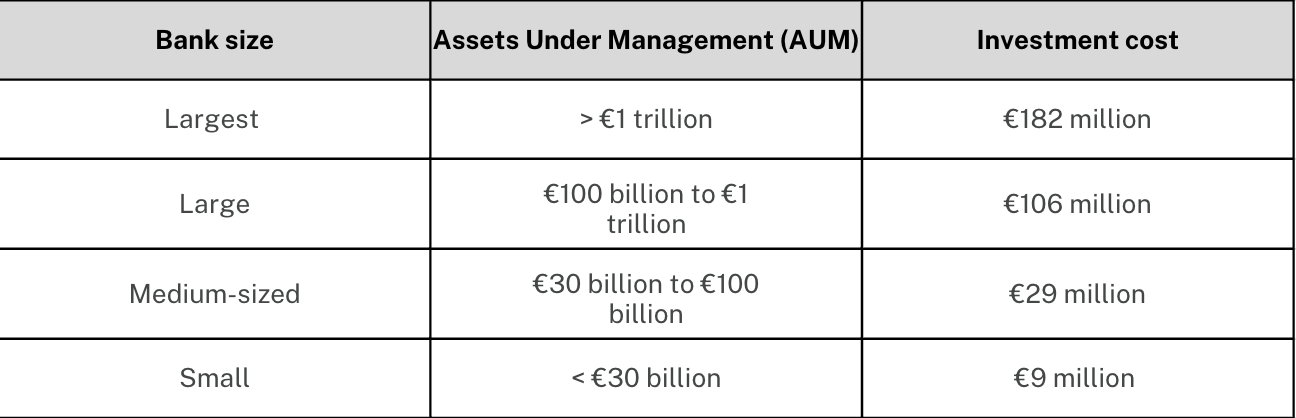

A cost study commissioned by the European Credit Sector Associations (ECSAs), which together represent the European banking sector, estimates an average initial cost of €110 million per bank. This does not even consider follow-up expenses such as operational, maintenance or offline-feature costs. The study distinguishes investment costs based on banks’ size, ranging from €9 million for small ones to €182 million for the largest ones. These were also the baseline assumptions that the ECB discussed in its report (see detailed table below).

Source: ECB, A view on recent assessments of digital euro investment costs for the euro area banking sector

The ECB’s estimates are significantly more conservative than industry numbers as the potential for banks to share infrastructure and create synergies was accounted for. While the definitive financial picture will only become clear as design details are finalised, ECB Executive Board member Piero Cipollone indicated that the required capital expenditure would average roughly 3% of a bank's annual IT maintenance budget. This statement is to be considered with caution, though, due to potential unanticipated or local costs. It is also often claimed that banks might incur significant revenue losses due to deposit shifts towards the Digital euro platform. Since the holding limit of digital euros by consumers should be set around a cap of €3000, this mitigates this risk. According to the ECB's latest simulation, a maximum of €699 billion could be withdrawn from Eurozone banks (8.2% of all retail deposits) in a worst-case scenario.

From Compliance Burden to Strategic Opportunity

Either way, shifting from one payment method to another does not directly bring new revenue for the banks while the Digital euro will create brand-new running costs. The provision of AI-driven value-added services such as conditional payments (e.g. pay-on-delivery) or smart refunds, can be leveraged by retail banks as a solution to create new revenue models and enhance customer loyalty. More generally, it is an opportunity to modernise their legacy systems in the age of AI and further pursue their ongoing compliance efforts with the latest regulations (EU AI Act, GDPR, etc.).

The required integration of the Digital euro into merchant systems is also a prime strategic opportunity for retail banking. While retail merchants face mandatory updates to their physical and virtual terminals with few natural incentives to do so, banks could bundle the Digital euro alongside Wero — the European bank-owned initiative which proposes a direct, card-free payment solution. This would offer merchants a highly attractive escape route from the costly transaction fees currently dictated by non-European card giants. More fundamentally, it would allow retail banks to reclaim control over the account-to-account (A2A) infrastructure and stop handing over a share of their transaction revenue to overseas intermediaries. Consequently, retail banks could safeguard their net margins even while offering merchants lower, more competitive fees.

While consumers seem to reap the most immediate benefits, notably from the enhanced privacy offered by the offline mode, they also face the challenge of managing an increasingly complex account ecosystem. The banks’ role here is to provide a frictionless, highly integrated front-end user experience (UX) within their proprietary digital channels, ensuring that the transition between commercial bank money and digital euros is completely seamless for the consumer. This would allow banks to remain the undeniable gateway for day-to-day consumer finance, thereby preempting the threat of disintermediation by public-sector applications.

All in all, the implications of the Digital euro initiative are not as daunting as one might first expect but require Belgian financial actors to be cautious and take the necessary steps. On the one hand, it brings innovative opportunities that can be beneficial in the long term. On the other hand, the project entails high costs and greater uncertainty overall. The traditional PSPs are the biggest losers. Banks and merchants can benefit from this transition if properly managed. Consumers are the most obvious winners. To end on a positive note, it is worth recalling the past experience of the SEPA project. Although it faced initial resistance and certainly required significant investments from market actors, today most of us will agree that it was for the better.

At Sailpeak, we are helping the Belgian financial sector to seamlessly navigate the digital transition with a core focus on AI. We complement this with strong expertise in business strategy, payments and digital journeys.

Sources:

https://www.ecb.europa.eu/euro/digital_euro/timeline/profuse/shared/pdf/ecb.deprep251010_a_view_on_recent_assessments_of_digital_euro_investment_costs_for_the_euro_area_banking_sector.en.pdf

https://www.ecb.europa.eu/euro/digital_euro/pilot/html/index.en.html

https://www.ecb.europa.eu/press/intro/news/html/ecb.mipnews260305.en.html

https://economic-research.bnpparibas.com/html/en-US/Digital-euro-cost-hide-another-11/10/2025,52974

Our insights

The Digital euro will require banks to rethink their infrastructure, payment strategy, customer experience, and AI-enabled service models. Sailpeak helps Belgian financial institutions navigate this transition by combining expertise in business strategy, payments, digital journeys, and AI. Contact us to explore how your organisation can prepare for the Digital euro and turn this initiative into a strategic advantage.

-min.webp)